OECD Economic Outlook, Interim Report March 2026

Testing Resilience

Introduction

The conflict in the Middle East is testing the resilience of the global economy.

The outlook is surrounded by high uncertainty and reflects the interaction of two opposing forces:

On the upside, growth is supported by strong momentum in technology-related investment and production, lower tariff rates than previously assumed, and carry-over from robust outcomes in 2025.

On the downside, the halt in shipments through the Strait of Hormuz and the closure and damage of some energy infrastructure has generated a surge in energy prices and disrupted the global supply of energy and other important commodities, such as fertilisers. This is raising costs, weighing on demand and adding to inflationary pressures.

Key figures

Key figures

Global growth remained resilient prior to the conflict, but rising energy prices and uncertainty now weigh on the outlook

Global GDP growth is projected to remain broadly stable at 2.9% in 2026 before edging up to 3.0% in 2027, sustained by robust technology-related investment and gradually lower effective tariff rates. However, the evolving conflict in the Middle East weighs on growth and generates significant uncertainty around global demand. These projections assume that the current energy market disruption is temporary, with prices easing from mid 2026 onward.

Higher energy prices will prolong global inflation

Inflation pressures will persist for longer with G20 inflation now expected to be higher in 2026 than previously projected, reflecting the surge in global energy prices. G20 inflation is projected to be 1.2 percentage point higher than previously expected in 2026 at 4.0%, before easing to 2.7% in 2027 with an assumed fading of energy price pressures. Core inflation in advanced G20 economies is expected to weaken, from 2.6% in 2026 to 2.3% in 2027.

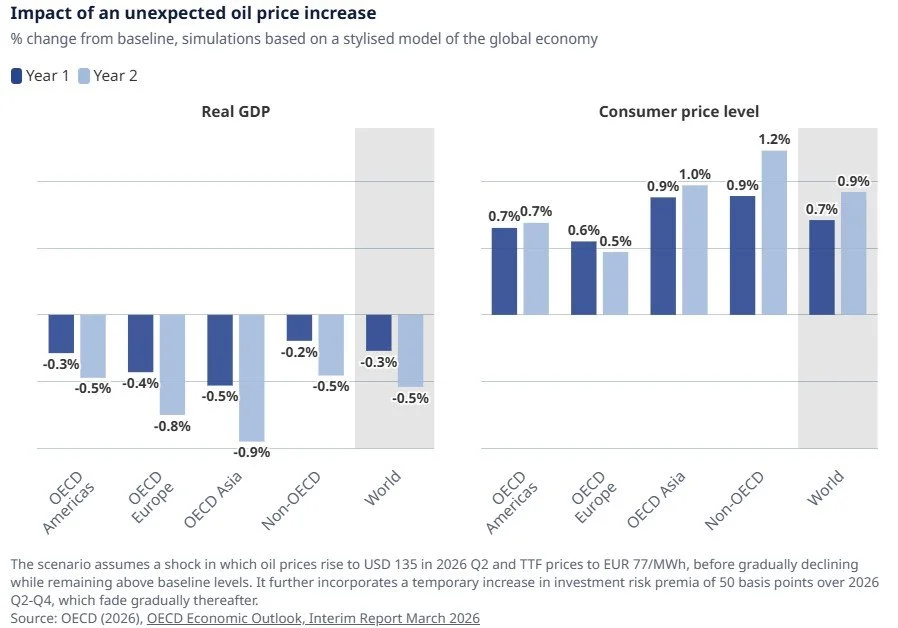

A further spike in energy prices would hit growth and inflation significantly

Market expectations point to a gradual decline in energy prices, an assumption underpinning current projections. However, a prolonged disruption to shipments through the Strait of Hormuz or sustained closures of oil and gas facilities could lead to significantly worse outcomes. Simulations in the report explore a scenario where oil and gas prices rise well above baseline projections - by around a quarter in the first year and remaining elevated thereafter - combined with tighter global financial conditions. In this case, global GDP could be around 0.5% lower by the second year, while consumer prices would be higher by about 0.7 percentage points in the first year and 0.9 percentage points in the second.

OECD (2026), OECD Economic Outlook, Interim Report March 2026: Testing Resilience, OECD Publishing, Paris, https://doi.org/10.1787/d4623013-en.