LCI Monthly – What Shaped February 2026

Economy & Politics

AI Disruption Reshapes the Software Sector: From Market Darlings to Margin Pressure

In early February 2026, the global software sector came under intense pressure as rapid advances in artificial intelligence reignited fears of structural disruption. New AI models and platforms—capable of writing, testing, and modifying software at very low cost—have triggered sharp sell-offs, particularly among highly valued software-as-a-service companies. Investors increasingly worry that corporate customers will use AI tools to replace or reduce spending on traditional software licenses, undermining revenues and pricing power. These concerns are already reflected in market performance. Software stocks have fallen sharply year to date, with notable losses among former market leaders. Segments such as compliance, research, legal, and creative software have been hit first, as AI-driven alternatives begin to replicate tasks once handled by specialized applications. Tools such as Anthropic’s Claude Legal highlight how quickly AI capabilities are improving, processing and cross-referencing hundreds of pages of complex documents—raising fears that parts of the software industry could become commoditized. At the same time, software companies face rising costs as they invest heavily in AI to stay competitive, while meaningful revenues from these new features remain limited. Even if revenue erosion is still years away, markets are already pricing in the risk. Despite the gloomy sentiment—described by some analysts as a “capitulation phase”—a total collapse of the sector appears unlikely. Complex enterprise software, particularly CRM and ERP systems, benefits from deep data integration, regulatory constraints, and customer lock-in that are difficult for AI newcomers to replicate. Data-centric platforms underpinning AI adoption are also seen as relatively resilient. Overall, AI is likely to compress margins and lower software prices, but it may also enable new applications and business models. Rather than a zero-sum threat, AI is reshaping the software landscape—favouring large, system-critical players with scale, proprietary data, and strong network effects.

China Challenges the Global Dominance of the U.S. Dollar

China is increasingly challenging the dominance of the U.S. dollar in global trade and finance. Through a combination of policy initiatives, China is promoting the international use of the renminbi (RMB), particularly in trade settlement, energy transactions, and cross-border investments. Bilateral agreements with key trading partners allow payments in local currencies, reducing reliance on the dollar. At the same time, China is expanding its own financial infrastructure, such as the Cross-Border Interbank Payment System (CIPS), as an alternative to the dollar-centric SWIFT network. Geopolitical tensions and the use of financial sanctions by the United States have accelerated this push, as China and other emerging economies seek to limit their exposure to dollar-based systems. China is also steadily diversifying its foreign exchange reserves away from U.S. Treasuries, while encouraging state-owned enterprises and commodity exporters to invoice in RMB. Despite these efforts, the dollar’s global dominance remains largely intact. Capital controls, limited financial market openness, and concerns over transparency and rule of law continue to restrict the renminbi’s appeal as a true reserve currency. Rather than a sudden overthrow of the dollar, China’s strategy points to a gradual move toward a more multipolar currency system, where the dollar remains dominant but faces growing competition at the margins.

Takaichi’s Landslide Opens the Door to a Historic Shift in Japan’s Geopolitics

Japanese Prime Minister Sanae Takaichi has achieved a historic political breakthrough, leading the ruling Liberal Democratic Party to a two-thirds majority only four and a half months after taking office. It is the strongest result in the party’s 70-year history and gives Takaichi unprecedented freedom to reshape Japan’s geopolitical role. Although the LDP performed less impressively in the proportional vote, the parliamentary supermajority could have far-reaching consequences for both foreign and domestic policy. Takaichi’s central aim is to prepare Japan for an era of intensified great-power rivalry and declining globalization. Despite very high public debt, she plans expansive fiscal policies to boost defence spending and strategic industries, seeking greater economic and geopolitical autonomy and stronger deterrence against China, particularly over Taiwan. Unlike her predecessors, she is no longer constrained by the more pacifist Komeito party, which has left the governing coalition. Security policy may shift rapidly, potentially breaking long-standing taboos such as hosting U.S. nuclear weapons or acquiring nuclear-powered submarines. Economically, markets initially welcomed her pro-growth agenda, with the Nikkei 225 surging, while the yen weakened on fiscal sustainability concerns. Domestically, Takaichi favors a stronger state and executive power, potentially at the expense of civil liberties, and may revive efforts to revise Japan’s pacifist constitution. Yet a fragmented and volatile party landscape suggests her long-term dominance is not guaranteed.

U.S. Supreme Court Limits Trump’s Emergency Tariff Powers, President Turns to Alternative Trade Laws

In February 2026, the Supreme Court of the United States ruled that Donald Trump had exceeded his authority with his tariff announcements. Trump had justified the tariffs by invoking an emergency powers law that allows a president to issue decrees in times of crisis without seeking approval from Congress. However, the Court’s decision does not apply to tariffs on specific products such as steel, aluminum, or automobiles. These remain in force because Trump based them on a different legal framework—Section 232 of the Trade Expansion Act of 1962. Trump responded immediately to the ruling, stating that he would use alternative measures to raise revenue. The following day, he increased global tariffs to 15 percent. This time, he relied on a trade law from 1974, which allows the president to impose tariffs on imports for up to 150 days. Any extension beyond that period would require congressional approval.

Nvidia Extends AI Lead with Strong Growth and Confident Outlook

Nvidia continues to benefit significantly from the global expansion of artificial intelligence, delivering quarterly revenue of $68.1 billion, above market expectations. The company forecasts further acceleration, projecting $78 billion in revenue next quarter, reflecting sustained demand for its AI-focused chips. Profit margins remain exceptionally high at around 75%, underscoring its dominant position in specialized AI hardware. A substantial share of revenue still comes from major cloud providers such as Amazon, Microsoft, Alphabet, Meta, and Oracle, which are collectively planning massive AI infrastructure investments this year. Nvidia has reassured investors that it can meet this demand. However, revenue expectations for China remain muted despite easing trade tensions. Although competition is intensifying—with companies like Google and AMD developing alternative AI chips—Nvidia maintains a strong ecosystem and broad customer base. With a market value near $4.7 trillion and a more moderate valuation multiple than in the past, Nvidia remains central to the ongoing AI investment cycle and appears well positioned for further growth.

The United States and Israel carried out large-scale military strikes against Iran, resulting in the reported death of Supreme Leader Ayatollah Ali Khamenei.

The operation marks one of the most dramatic escalations in Middle Eastern tensions in decades. Washington has justified the action by citing the need to halt Iran’s alleged nuclear ambitions, curb its missile development, deter threats to U.S. forces and allies, and respond to human rights abuses. However, many analysts argue that these explanations do not clearly establish the presence of an immediate or unavoidable threat. Iran has long denied pursuing nuclear weapons, and previous international assessments indicated that any structured weapons program had ended years ago. While concerns about uranium enrichment persist, evidence of an imminent nuclear breakout remains contested. Critics contend that invoking nuclear risks in this context reflects a familiar pattern of preventive logic, where perceived future dangers are used to justify present military action. Others view the strikes as aligned with broader strategic objectives, including weakening Iran’s regional influence, reinforcing Israeli security priorities, or indirectly encouraging regime change. Legal scholars and diplomats have questioned both the proportionality and long-term wisdom of such an escalation, warning that it may increase instability rather than enhance security. In sum, while the operation is framed as defensive, its strategic rationale remains widely debated.

Middle East Conflict Triggers Major Shock to Global Oil Markets

The escalating conflict between the United States, Israel, and Iran has triggered the most severe shock to global energy markets in decades. Although no confirmed physical damage to major oil and gas infrastructure has been reported, the uncertainty alone is disrupting flows from the Gulf region, which accounts for roughly 20% of global oil supply. Brent crude had already climbed toward $70 per barrel prior to the strikes, and further price increases are expected. Explosions were reported in several Gulf states, and tensions are centered on the Strait of Hormuz, through which nearly 20 million barrels per day transit. While shipping has not been formally halted, some energy companies and traders have suspended movements due to security risks. Tanker freight rates have surged sharply, reflecting heightened danger and limited vessel availability. Global supply conditions are stronger than in past crises, with increased production from the U.S., Brazil, and Canada, and higher exports from Saudi Arabia. However, even temporary disruptions in Gulf shipping routes could significantly tighten markets and amplify price volatility.

Markets

Global Overview

Global equities gained 0.8% in February (+1.1% in EUR terms and +0.2% in CHF terms). Performance was particularly strong in Europe and parts of Asia, while U.S. equities were broadly flat over the month. Fixed income markets remained relatively stable, with government bond yields and credit spreads mostly unchanged. Amid ongoing geopolitical tensions, gold rose by 15%, reflecting increased demand for safe-haven assets.

Europe

Europe had its second consecutive month of strong gains, rising 4% in February and outperforming global peers. All sectors were up in February with the exception of Financials. Communication Services and Real Estate led the way, delivering double-digit returns. Best performers were UK +6.7%, France +5.9% and Switzerland +5.7%. Eurozone Equities were up 3.2%.

On the fixed income side, sovereign bonds in most European countries had positive returns. Switzerland, the lowest yielding country, was the lone exception. European corporate bond returns were also positive, but in general they underperformed government debt.

North America

February proved difficult for U.S. equity markets. Increased investor attention on the scale of AI-related investment spending and its implications for corporate profitability weighed on large-cap stocks, contributing to a third consecutive weekly decline for the S&P 500. Toward month-end, a higher-than-anticipated producer price index reading reignited concerns about inflation and reduced expectations for imminent Federal Reserve rate cuts. As a result, the S&P 500 finished the month approximately 0.8% lower.

Market dynamics shifted during the period, with smaller companies outperforming their larger counterparts. Mid Caps gained roughly 4%, while the Small Caps advanced about 2%. Within large caps, sector performance was uneven, reflecting a moderation in enthusiasm around mega-cap technology stocks and a renewed preference for more defensive areas. Utilities posted strong gains of around 10%, whereas Communication Services and Consumer Discretionary sectors ended the month in negative territory.

In fixed income markets, conditions were generally supportive. The yield on the 10-year U.S. Treasury declined below 4% for the first time since November, as investors moved toward safer assets amid concerns about slowing growth combined with persistent inflation pressures.

Canada had a solid performance, +6.9%.

Latin America

Latin American equities also delivered solid performance. Mexico rose by 6.3%, leading the region, while Brazil gained 1.4% over the month.

Asia-Pacific

Asia Pacific equities extended their positive momentum and outperformed global peers in February, rising 7% to an all-time high, led by developed markets.

South Korea topped the region again, surging 22% (up 56% YTD). Thailand, Taiwan, and Japan also outperformed the regional benchmark, posting double-digit returns. Meanwhile, China lagged, down 7%, held back by soft consumption data from the Lunar New Year holidays (all returns in local currency terms).

All regional fixed income indices advanced; the local-currency Asian Local Bond climbed 2%, compared to a 1% gain in the USD-denominated USD Asia-Pacific.

Japanese equities surged in February as Prime Minister Sanae Takaichi's snap-election win boosted market sentiment. The Japan 500 finished up 11% at a record high. 10 out of 11 sectors rose, with 7 posting double-digit gains. Real Estate led, jumping 20%. Communication Services was the sole decliner, dragged by revenue shortfalls. Japanese bonds stabilized as Takaichi calmed debt issuance fears, further supported by the U.S. Supreme Court overturning Trump's tariffs. The Global Government Japan rebounded 2%, currently yielding 2.49%.

Australian +5.8% rose in February hitting a new all-time high.

Learn more on LCI Research

Equity Performance of selected Countries

Equity Markets in Local Currency

Equity Performance of Global Sectors

Equity Global Sectors in USD

Learn more about LCI Strategies

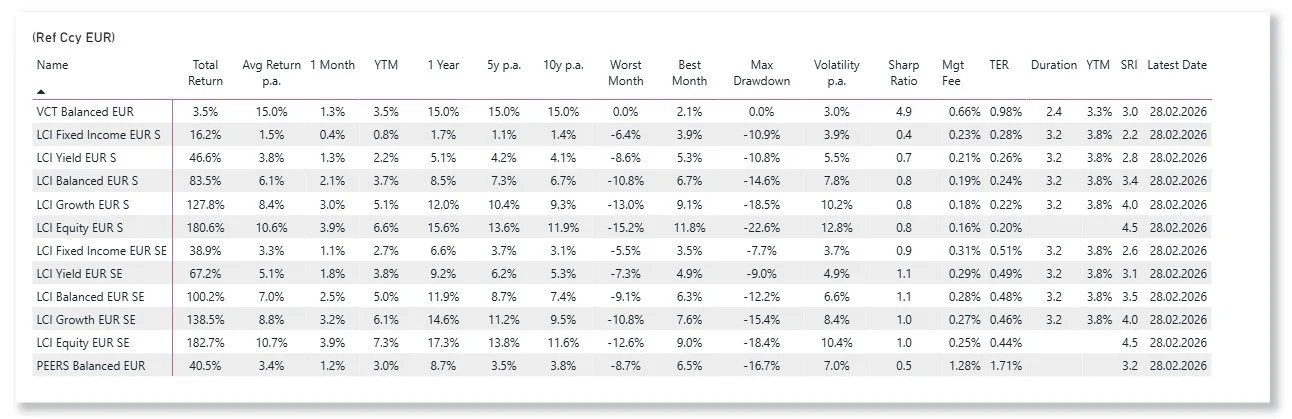

LCI Strategies Performance update

LCI Strategies in CHF, EUR and USD