LCI Monthly – What Shaped March 2026

Economy & Politics

Q1 2026: Geopolitics, Rate Shocks and Market Dislocation

The first quarter of 2026 was marked by exceptional volatility, driven primarily by geopolitical tensions and rapidly shifting macroeconomic expectations. The escalation of the Iran conflict triggered a sharp sell-off in global equities, while energy markets surged—oil prices recorded one of their strongest quarterly increases in decades and European gas prices rose significantly. At the same time, interest rate expectations reversed abruptly, with yields rising across major economies and raising concerns about a stagflationary environment.

This backdrop weighed heavily on growth sectors, particularly large technology companies, and disrupted momentum in emerging markets. Traditional diversification offered only limited protection: while the U.S. dollar strengthened, gold and government bonds both declined, reflecting the unusual nature of the current regime.

Beyond the Middle East, markets were already unsettled by broader geopolitical and political uncertainties. Asset price movements were unusually volatile and at times inconsistent, with sharp rallies and reversals across equities, commodities, and credit markets. Currency markets also came under pressure, particularly in energy-importing economies, while cryptocurrencies remained highly volatile. Overall, investors face a complex and uncertain environment, with geopolitical risks, policy shifts, and upcoming elections likely to sustain elevated volatility in the months ahead.

Iran War: Tactical Gains, Strategic Uncertainty

Since the initial phase of the conflict, the conventional military balance has remained tilted toward Israel and the United States. Iran’s command structure and infrastructure have been significantly degraded, limiting its ability to project large-scale force. However, the conflict has evolved into a more asymmetric and economically disruptive phase rather than moving toward resolution.

Iran has avoided direct large-scale confrontation while intensifying indirect pressure. Risks around the Strait of Hormuz remain elevated, leading to persistent disruptions in shipping flows, higher insurance costs, and sustained pressure on energy prices. While a full blockade has not materialized, intermittent incidents and rising risk premiums have kept oil markets tight and volatile.

Politically, the Iranian regime has proven more resilient than initially expected. Although weakened, it remains in control and continues to reject ceasefire conditions that could be perceived as capitulation. Its nuclear posture remains deliberately ambiguous, preserving strategic leverage.

For the United States, the situation has become increasingly complex. Domestic support for prolonged engagement remains limited, and policymakers are constrained between escalation risks and the perception of strategic retreat. At this stage, no clear endgame is visible. The conflict has effectively shifted from a short-term military confrontation to a prolonged geopolitical standoff with lasting implications for energy markets and global risk sentiment.

Strategic Oil Reserve Release Cannot Solve the Hormuz Crisis

In response to the disruption of Middle Eastern energy flows, industrialized countries have agreed to release approximately 400 million barrels of oil from strategic reserves—one of the largest coordinated releases on record. The decision by the International Energy Agency (IEA), which comprises 32 member countries, aims to stabilize global energy markets as tensions around the Strait of Hormuz intensify. The strait typically accounts for roughly 20% of global oil shipments.

Since the escalation of the conflict and the severe disruption to shipping flows, oil prices have risen sharply. Brent crude has moved above USD 100 per barrel, roughly 50% higher than pre-conflict levels, reflecting fears of prolonged supply constraints.

However, the reserve release cannot immediately replace lost supply. Oil must be extracted, sold, and physically distributed—a process that takes time. Meanwhile, tanker traffic through the Strait remains significantly reduced due to security concerns, including potential attacks and mining risks.

As a result, despite the massive reserve release, markets remain tense, highlighting that reopening the Strait of Hormuz remains the key to restoring stability in global energy markets.

Fed Holds Rates as War-Driven Inflation Clouds Outlook

The Federal Reserve kept its policy rate unchanged at 3.5–3.75%, adopting a cautious, wait-and-see approach amid heightened uncertainty. Oil prices above USD 100 per barrel are already feeding into inflation, with gasoline prices rising and producer prices surprising to the upside.

Chair Jerome Powell emphasized that the duration and persistence of the energy shock remain unclear. While such shocks are often temporary, there is a growing risk that inflation expectations could become more entrenched, potentially requiring further tightening. Expectations for rate cuts have diminished significantly, with many policymakers now anticipating little or no easing this year.

At the same time, growth risks are increasing as higher energy costs weigh on consumption. The Fed faces a difficult balancing act between containing inflation and supporting economic activity, while also navigating political pressure.

ECB on Hold as War-Driven Inflation Risks Re-Emerge

The European Central Bank kept its deposit rate unchanged at 2%, but the macro outlook has shifted. Following the escalation in the Middle East, inflation forecasts were revised upward to 2.6% for 2026 and 2.1% for 2027, while growth projections were lowered to 0.9%.

Although inflation had recently stabilized near target, rising oil and gas prices—driven by disruptions around the Strait of Hormuz—are increasing upside risks. Additional pressures may come from higher food prices and renewed supply chain constraints.

President Christine Lagarde reiterated that the ECB stands ready to act if inflation proves more persistent. Markets are now pricing in the possibility of renewed tightening later in 2026, depending on how energy shocks feed through to the broader economy.

Brent

Markets

Global Overview

Global equities declined by 6.3% in March 2026 (–4.4% in EUR terms and –2.9% in CHF terms), weighed down by escalating geopolitical tensions and a renewed surge in energy prices. Oil-importing economies—particularly in Asia and Europe—were more adversely affected than the United States. The USD appreciated by around 2% against the EUR.

In fixed income markets, yields rose broadly, reflecting higher inflation expectations and a reassessment of the interest rate outlook.

Gold prices fell by approximately 10%, driven by the unwinding of speculative positions and the prospect of higher real rates.

Europe

European markets were particularly hard hit, with equities falling by roughly 9% over the period. This decline erased all gains accumulated since the start of 2026 and pushed markets into negative territory. Disruptions around the Strait of Hormuz drove a sharp increase in energy prices, weighing heavily on economic sentiment.

Most sectors declined significantly as higher input costs and uncertainty dampened activity. Real estate was especially affected, dropping around 17%, reflecting its sensitivity to rising yields and tighter financing conditions. In contrast, the energy sector benefited from the price surge, advancing by approximately 22% and standing out as the only major area of strength.

Sovereign bond markets also came under pressure, with rising inflation expectations and higher yields leading to negative quarterly returns across both core and peripheral markets.

North America

U.S. equities experienced a volatile first quarter, pressured by tariff uncertainties, renewed concerns around AI, and tensions in private credit markets. Sentiment deteriorated in March as the Middle East conflict revived stagflation fears and reduced expectations for Fed rate cuts. Although markets rebounded on the final trading day, U.S. equities still ended the quarter down around 4% (–4.9% in March), marking the weakest performance since Q3 2022.

The rotation into smaller companies continued, but mid- and small-cap stocks were not immune to the March sell-off, even if they remained positive over the quarter. Sector performance diverged significantly: Energy surged on higher oil prices, while technology-related sectors and financials recorded notable declines.

Fixed income markets also struggled, with rising yields pushing bond indices into negative territory.

Latin America

Brazil and Mexico proved relatively resilient compared with most Asian and European markets. Mexico declined by 3.9% in March but still delivered a gain of 8.1% for the quarter. Brazil performed even better, slipping just 0.9% over the month and ending Q1 up 12.7%, supported by stronger domestic dynamics and commodity exposure.

Asia-Pacific

Japanese equities declined by around 10% in March, reflecting the impact of higher energy prices, but still ended the quarter up approximately 3%.

South Korean markets corrected sharply, falling around 20% in March, yet remained strong overall with gains of roughly 24% for the quarter. In contrast, India and Indonesia both posted notable declines, falling 11.3% and 14.4% in March, bringing their year-to-date performances to –13.6% and –18.9%, respectively. Chinese equities declined by 7.4% over the month and were down approximately 10.4% for the quarter.

Learn more on LCI Research

Equity Performance of selected Countries

Equity Markets in Local Currency

Equity Performance of Global Sectors

Equity Global Sectors in USD

Learn more about LCI Strategies

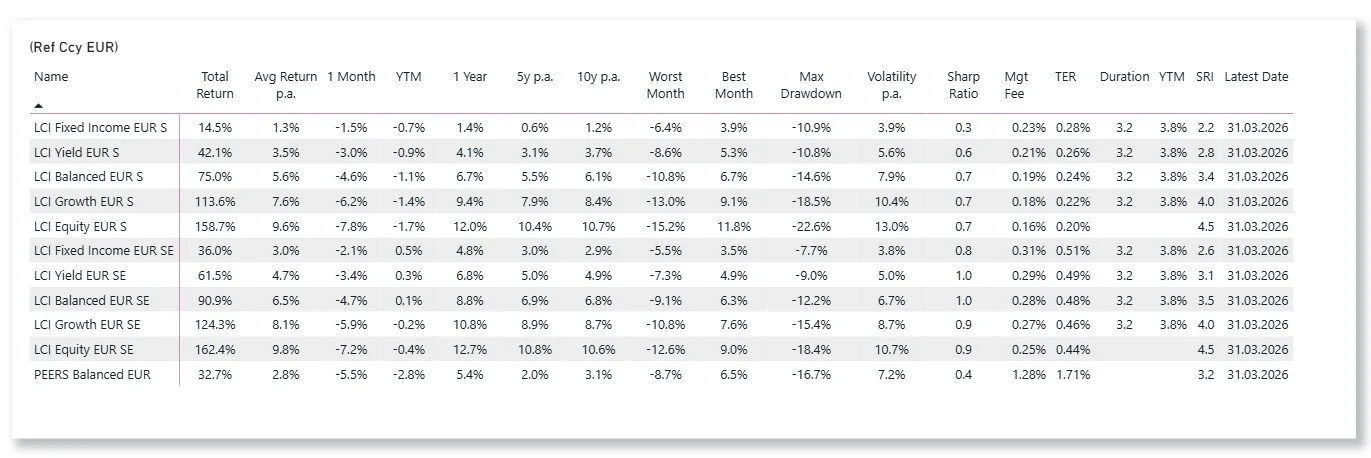

LCI Strategies Performance update

LCI Strategies in CHF, EUR and USD