LCI Monthly – What Shaped April 2026

Economy & Politics

Iran War: Ceasefire, Negotiations, and Strategic Deadlock

April marked a critical inflection point in the conflict. After the initial ceasefire declared on April 8th, fighting continued in a fragmented and asymmetric form — with Iran maintaining pressure through missile strikes on Gulf states, closures of the Strait of Hormuz, and proxy activity across the region. Pakistan emerged as a key mediator, hosting preliminary talks between Washington and Tehran, though progress remained elusive. On April 21st, President Trump extended the ceasefire at Pakistan's request, but by April 25th, he cancelled U.S. negotiators' participation in further rounds, citing insufficient Iranian movement. Iran's parliament simultaneously signalled it would not negotiate under threat. The death of several senior IRGC commanders in joint U.S.–Israeli strikes further complicated the political landscape. As of month-end, no clear endgame is visible — the conflict has shifted from an acute military confrontation into a prolonged geopolitical and economic standoff.

IMF World Economic Outlook: Growth Revised Down, Inflation Up

The IMF's April 2026 World Economic Outlook, published under the title "Global Economy in the Shadow of War", delivered a sobering assessment. Global growth was revised down to 3.1% for 2026 and 3.2% for 2027 — well below the pre-pandemic average of 3.7%. The primary drivers of the downgrade are the Middle East conflict and its knock-on effects on energy prices, inflation, and financial conditions. Global headline inflation is expected to tick up in 2026 before resuming its decline in 2027, complicating the path for central banks. Emerging markets and commodity-importing economies face the sharpest deterioration. The IMF highlighted several compounding risks: a broader or longer conflict, renewed trade tensions, and eroding credibility of fiscal and monetary institutions. Policy-driven fragmentation of global trade was also flagged as a structural headwind to long-term growth.

Hungary: The End of the Orbán Era

April's most significant European political event was the defeat of Viktor Orbán in Hungary's parliamentary election — a result few observers had considered likely even months ago. Péter Magyar's Tisza Party secured a landslide victory, ending 16 years of Fidesz–KDNP rule and fundamentally reshaping Hungary's political landscape. Magyar, a former insider who turned into Orbán's most effective critic, campaigned on anti-corruption, rule of law, and a clear pro-European platform. The result marks a dramatic reversal for one of the EU's most contentious member states and is likely to accelerate Hungary's re-engagement with European institutions, including on the rule of law conditionalities that had frozen EU funding. Combined with the parallel victory of the left-wing Progressive Bulgaria coalition, April signalled a broader shift in Central and Eastern European politics, with voters increasingly rejecting entrenched nationalist governments.

Earnings and the AI Trade Override Geopolitical Noise

April delivered a striking contradiction: financial markets rallied as the Iran war ground on. The key driver was a robust corporate earnings season, with approximately 80% of S&P 500 companies reporting Q1 results that exceeded analyst expectations. Alongside solid profits, the artificial intelligence investment theme returned to the fore, reigniting appetite for technology stocks that had sold off sharply in Q1. The announcement of an indefinite ceasefire extension provided an additional catalyst, easing the most acute tail risks for energy markets. Investor sentiment appeared to compartmentalise geopolitical uncertainty, focusing instead on fundamentals. This divergence is not without risk — consumer confidence remains fragile, labour market conditions are softening, and real household purchasing power continues to erode under elevated energy costs. Yet for now, the market appears to be looking through short-term disruption, prioritising earnings visibility over macro headwinds.

OPEC Splits: The UAE Walks Out of the Cartel

In a structural break for the oil cartel, the United Arab Emirates announced their departure from OPEC effective May 1st. Abu Dhabi, which holds the bulk of the country's reserves, had been a member since 1967 and lifted output from under 400,000 barrels per day to roughly 4 million by 2024, making the UAE the cartel's third-largest producer behind Saudi Arabia and Iraq. The official rationale cites a need for greater flexibility and a sharper focus on national interests, after years of accepting restrictive quotas. The timing looks opportunistic: while the Iran war keeps tanker traffic through the Strait of Hormuz largely blocked, the alternative pipeline capacity to the Gulf of Oman is limited — but once shipping resumes, Gulf producers with spare capacity stand to capture both running demand and the global restocking that follows. Political frustration also plays a role: senior diplomatic advisor Anwar Gargash criticised what he viewed as insufficient political and military backing from neighbouring Gulf states. The exit further weakens OPEC's pricing power at a time when discipline within OPEC+ had already been fading, and benefits the United States, now the world's largest oil producer thanks to shale.

Fed Holds Rates at 3.5–3.75% as Powell Bows Out Amid Inflation Risks

In what proved to be Jerome Powell's final policy decision as Federal Reserve Chair, the FOMC voted to keep the benchmark rate unchanged at 3.5–3.75%. The decision reflects mounting caution as the Iran conflict pushes energy prices higher, threatening to reignite inflation. The committee remains divided: Trump-appointed Governor Stephen Miran pressed for a 25 basis point cut, while three voting members dissented on the statement's dovish lean, signalling that a hike may yet be required this year.

In a notable twist, Powell announced he will not vacate his Board of Governors seat after handing the chair to Kevin Warsh in mid-May. He intends to remain in a non-executive capacity until the political and legal pressures on the institution fully subside — a move likely to frustrate the White House and underscore his commitment to defending Fed independence. Markets dipped slightly on the cautious inflation language. Stagflation fears persist, though Powell argues current conditions remain far from the 1970s precedent, with unemployment still low at 4.3%.

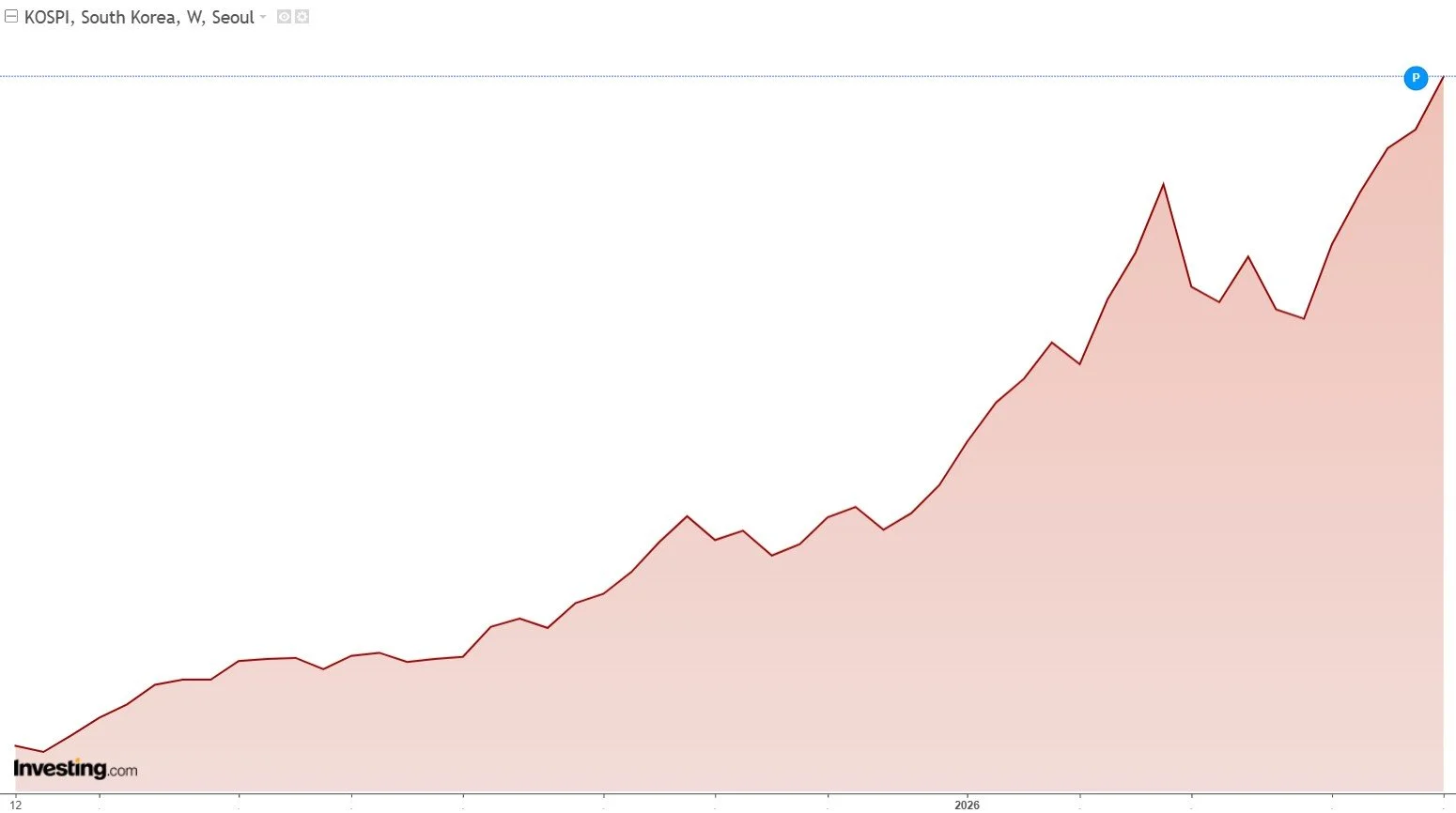

Kospi

Markets

Executive Summary

April 2026 delivered one of the most powerful monthly equity rallies of the cycle. The MSCI World gained +9.6% in USD as investors looked through a deteriorating geopolitical backdrop – an open US–Iran confrontation, a partially disrupted Strait of Hormuz and an oil-price spike – and chose instead to focus on a spectacular wave of AI-related capital expenditure, a strong Q1 earnings season and the prospect of an eventual Fed easing cycle.

The dispersion across markets was extreme: South Korea (+33.9% in local currency) and the global IT sector (+19.3% in USD) drove the headlines, while Latin America, Indonesia and the global Energy sector lagged. Fixed-income returns were modest but uniformly positive, with credit and emerging-market debt outperforming sovereigns thanks to spread tightening.

Equity Markets – Regional Performance

1-month returns in local currency

Europe

Europe was a clear second tier relative to North America and Asia. The Eurozone (+6.9%) was led by Italy (+7.9%) and Germany (+6.8%), both of which benefited from cyclical and industrial exposure, with German autos and industrials in particular helped by improving export-earnings expectations.

France (+4.2%) trailed, weighed down by luxury, while Switzerland (+4.1%) was held back by its heavy defensive tilt – Nestlé, Roche and Novartis together account for roughly half of the SMI – which structurally underperforms in a tech- and AI-led cyclical month, with a firmer CHF adding a further drag on multinational exporters. Spain (+5.3%) held up well on the back of strong bank earnings.

The United Kingdom (+2.5%) was the developed-market laggard – its structural tilt to defensives and the surprising weakness in Energy left it with little participation in the AI-driven rally.

North America

The US (+10.5%) delivered its strongest month since 2020, led by the Magnificent Seven and a broad re-rating of semiconductors and AI infrastructure plays. Q1 earnings beat expectations, with the blended growth rate above 13% y/y and IT companies tracking towards roughly 38% earnings growth for the full year.

Canada (+4.4%) lagged the US, hampered by softer commodity exposure outside oil.

Latin America

Latin America was the soft spot. Brazil (-0.4%) and Mexico (-0.4%) both ended in negative territory despite still-attractive valuations (Brazil P/E 10.9, EY 9.2%). Local political uncertainty and currency pressures more than offset the global tailwind. Indonesia (-5.3%) suffered the worst monthly decline in the universe, on a combination of capital outflows from non-AI EMs and weaker commodity exposure.

Asia-Pacific

The standout was South Korea (+33.9%), posting its best month in 28 years. The KOSPI rally was almost entirely an AI memory-chip story: Samsung Electronics and SK Hynix together drove the index, with SK Hynix up around 60% on the month and Samsung up roughly 35%. South Korea's total market capitalisation crossed USD 4 trillion, briefly overtaking the United Kingdom to become the world's eighth-largest equity market.

The same theme propelled India (+9.2%), where IT services and chip-design exposure benefited from the global AI capex surge, and to a lesser extent China (+2.8%), where the rally was held back by ongoing property-sector concerns. Japan (+7.5%) delivered a solid month, helped by yen weakness and a positive read-through from the AI rally to its semiconductor-equipment names. Australia (+2.0%) was muted, held back by its bank- and resources-heavy composition.

Equity Markets – Sector Performance

1-month returns in USD

IT (+19.3%) and Communication Services (+15.4%) dominated, both lifted by AI capex announcements and stronger-than-expected hyperscaler earnings. The Philadelphia Semiconductor Index rose close to 40% on the month, and Intel's Q1 print sent its shares up by more than 23% in a single session – its best day since 1987.

Consumer Cyclicals (+9.5%) and Industrials (+9.0%) rounded out the leadership, supported by improving earnings revisions and resilient consumer data. Financials (+7.3%) benefited from a still-steep yield curve and constructive Q1 bank results. The rest of the market participated only modestly: Materials +4.2%, Utilities +3.2% and Consumer Staples +3.0%.

The two negatives were instructive. Energy (-1.9%) ended the month lower despite the surge in spot oil, as investors took profits after the sector's strong YTD run (+35.4%) and questioned how durable a war-driven price spike could be. Health Care (-0.3%) was the weakest of the defensives, pressured by ongoing US drug-pricing rhetoric and a heavy pipeline of policy headlines.

Valuations across sectors are now stretched: IT trades at 31.6× forward earnings and Consumer Cyclicals at 32.1×, against ~14× for Financials – a reminder that the AI thematic carries both the performance and the valuation risk into the next quarter.

Fixed Income

Bond markets were quietly constructive in April. The asymmetry between sovereign and credit performance was the main feature.

USD Bonds

US Treasuries returned 0.1% on the month as long-end yields drifted higher on the energy-driven inflation impulse, leaving the YTM around 4.3%. Credit fared better: Corporate IG USD +0.4% (YTM 5.2%) and High-Yield USD +1.7% (YTM 6.9%), both helped by spread compression as risk appetite improved.

EUR Bonds

Returns were uniformly positive. Eurozone government bonds +0.3% (YTM 3.2%), EUR Corporate IG +1.0% (YTM 3.6%) and EUR High-Yield +2.0% (YTM 5.3%). The market shrugged off the inflation print and remains comfortable that the ECB will stay on hold.

Emerging Market Debt (USD)

EM debt was the strongest of the three blocks: EM Sovereign +2.0% and EM Corporate +1.6%, with current YTMs of 5.8% and 5.9% respectively. EM debt benefited from a softer USD, the broader risk-on tone and the AI-driven optimism toward Asian issuers.

The takeaway for the asset-allocation discussion is unchanged: in a world where sovereign duration provides only modest carry and is increasingly correlated with energy-driven inflation surprises, credit – and particularly EM and high-yield carry – remains the better-paid leg of fixed income.

Outlook

May begins with risk assets at or near record highs and with implied volatility once again low – a reminder that a great deal of good news is now in the price. The two near-term catalysts to monitor are:

(i) Any de-escalation or escalation in the Middle East and the corresponding move in oil;

(ii) The transition at the Fed, where Kevin Warsh's arrival could shift the balance of the committee toward earlier cuts.

Learn more on LCI Research

Equity Performance of selected Countries

Equity Markets in Local Currency

Equity Performance of Global Sectors

Equity Global Sectors in USD

Learn more about LCI Strategies

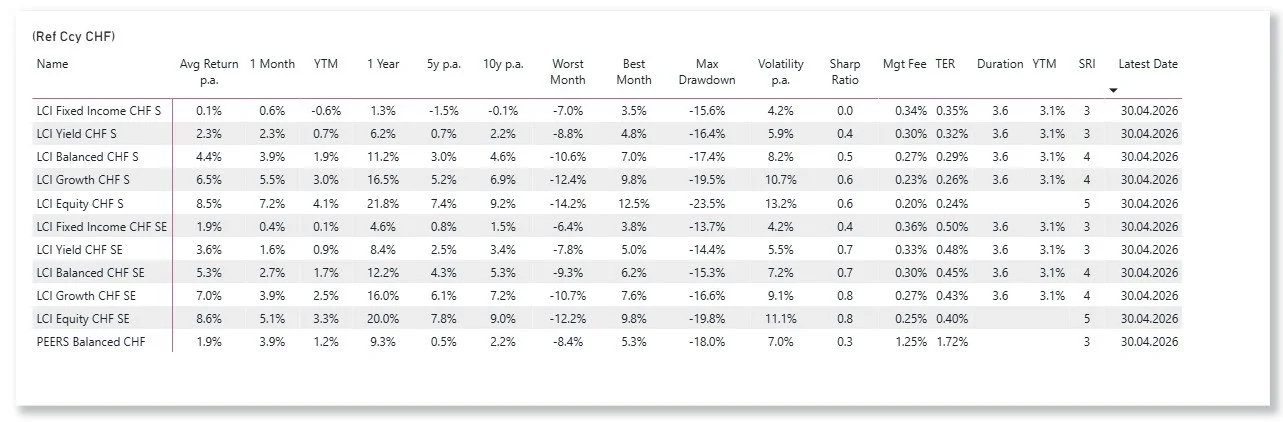

LCI Strategies Performance update

LCI Strategies in CHF, EUR and USD