OECD Economic Outlook – June 2026

Under Pressure

Introduction

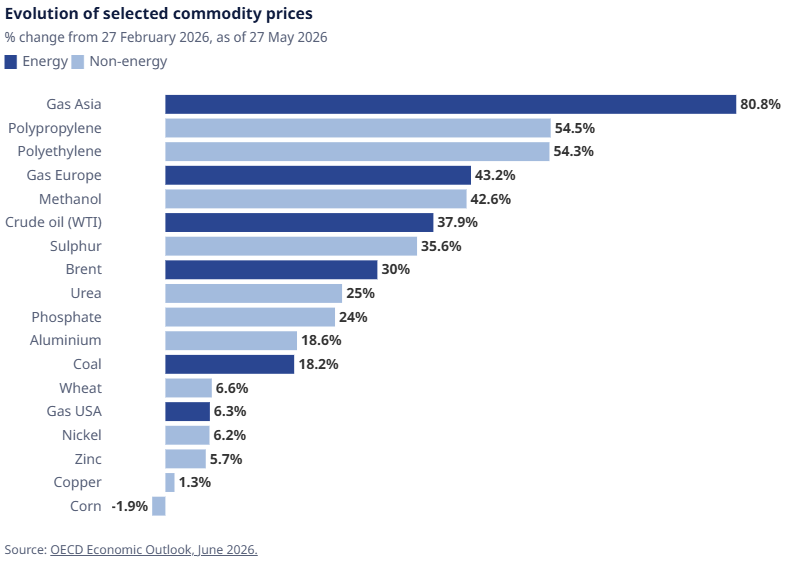

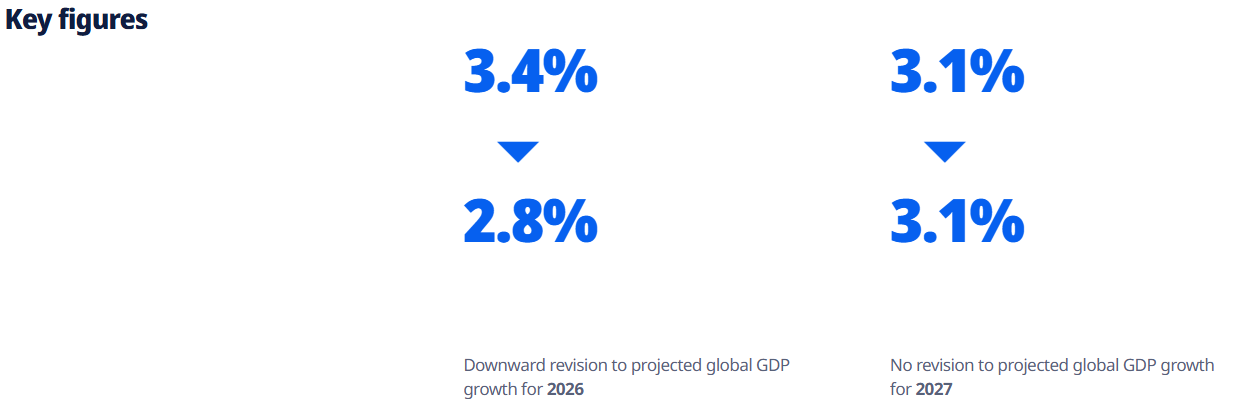

The conflict in the Middle East has become the dominant force shaping the global economic outlook. Energy prices and the prices of other key agricultural and industrial inputs produced in the Persian Gulf economies have soared since February as production and exports have been curtailed. This has been pushing up inflation, putting pressure on real incomes and economic growth. GDP growth projections have been revised down, while inflation has been revised up.

The longer the disruptions last, the larger the economic and social costs become

The duration and extent of the conflict remain uncertain, but the economic effects are likely to be felt for some time given the months it will take to restore damaged infrastructure and transport routes and deliver products around the world.

In light of the uncertainty, the Economic Outlook provides two scenarios for the global economy.

In a time-limited disruption scenario, the sizeable disruptions are assumed to remain relatively short-lived, while in a prolonged disruption scenario, broader disruptions last well into 2027, much longer-lasting negative consequences. Both scenarios occur against a background of an otherwise solid underlying momentum in the global economy, with output boosted by strong AI-related investment, production and trade, lower tariff barriers and supportive financial and fiscal conditions.

Global growth will weaken in the time-limited disruption scenario

Growth is set to slow modestly in North America and Europe before a tentative recovery, with the United States easing to 2.0% in 2026 and 1.8% in 2027, Canada dipping to 1.2% before rebounding to 1.7%, Mexico strengthening to 1.9% by 2027, the United Kingdom from 0.9% to 1.1%, while China moderates steadily to 4.5% in 2026 and 4.3% in 2027.

A prolonged disruption would weigh on growth and significantly raise inflation

In the prolonged disruption scenario, impacts would vary across regions, with energy‑importing Asian economies particularly exposed given their reliance on supplies from the Gulf.

More broadly, higher energy prices, supply shortages, tighter financial conditions and weaker confidence would weigh on activity worldwide. Inflation would also intensify, rising by around 0.4 percentage points in 2026 and 1.3 percentage points in 2027 – creating difficult trade-offs for policymakers, especially central banks.

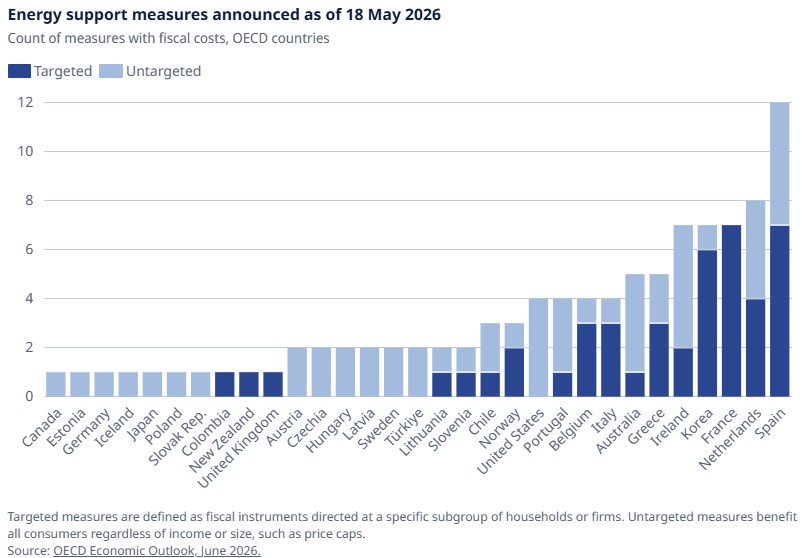

Many countries have acted quickly to provide energy price relief

Many governments have already implemented support measures for households and firms to mitigate the impact of higher energy costs. Such discretionary measures should be well-targeted on the households most in need and viable firms, preserve incentives to lower energy use and have clear expiry mechanisms, allowing prompt withdrawal as energy prices subside.

OECD (2026), OECD Economic Outlook, Volume 2026 Issue 1: Under Pressure, OECD Publishing, Paris, https://doi.org/10.1787/2d1956f0-en.

La Côte Invest Takeaway

For investors, the OECD’s two-scenario framing is a reminder that portfolios should be built to withstand a range of outcomes rather than a single forecast. With inflation revised up and energy the central swing factor, we continue to favour genuine diversification so that no single shock dominates a client’s results.

In practice, that means staying invested to capture the solid underlying momentum the OECD still sees, while keeping inflation sensitivity in check: measured duration in fixed income, exposure to real and inflation-resilient assets, and an active overlay that can lean against energy-driven volatility if the prolonged-disruption scenario materialises. As always, the right balance depends on each client’s objectives and risk profile — we calibrate positioning to those, not to headlines.